Excerpted from Neil’s latest book LandBook Second Edition: An Owner’s Manual for Rural Land

~~~~~~~~

If you’ve ever borrowed money then you’ve had occasion to regret the amount of your lifestyle that was going to pay interest on your loan.

Nobody likes to pay interest, but chances are, unless you were born very, very rich or very, very poor, you are currently paying interest to someone on a loan for something.

We don’t need to beat ourselves up over that. Because, without borrowed money, how many of us would have an education? How many would have a vehicle that starts every morning? How many would own a home? How many could buy land?

Interest then, is the penalty that we pay for not being very, very wealthy, or very, very destitute.

Once we have accepted that trauma, we can move on to ask ourselves what can be done to minimize our exposure to interest, and as luck would have it, there are a several ways to make it easier to pay most any note off in reduced time at less expense and without adding too great a financial burden. I’m going to show you three.

That’s not to say that the methods I’m about to demonstrate are any sort of free lunch, they aren’t. You pay interest for the use of someone else’s money, and these techniques work because you “rent” less of their money for a shorter period of time, i.e. you don’t have as much borrowed or borrow it for so long.

Here are three ways to accelerate the payment of almost any amortized loan (almost, because some lenders don’t allow you to make pre-payment) and each one is designed to reduce your interest charges, and have your note paid off as soon as possible in an affordable manner that has the least negative impact on your lifestyle.

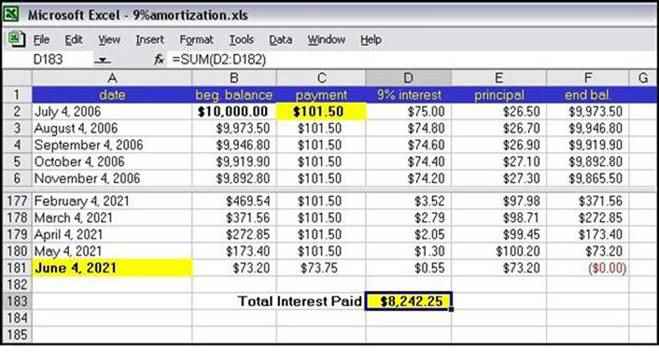

All of the examples I’ve provided here are based on a typical 15-year loan of $10,000 bearing annual interest at the rate of 9% per year (per annum). (To manage your interest payments, you’ll need an amortization schedule. If you don’t want to make your own, you can find a few hundred thousand of them if you do an internet search on “free amortization schedule”.)

Here’s what an amortization schedule for our typical loan will look like:

In the top part of the window, you see the total amount borrowed, $10,000, and the computations for principle and interest are figured with each successive payment. Notice that the first month, when you make your first payment of $101.50, only $26.50 of your payment goes toward your equity—that is, to decrease your debt—and the rest, about 75%, goes to interest. Note that this situation gets progressively better with each succeeding payment so that fifteen years later, at the end of the loan (the bottom part of the window) almost all the payment goes toward equity with almost none of it going to interest.

It’s important to note that the more extra principal (the part of your payment that goes to reduce your debt) you pay at the beginning of your loan, the more you save. Paying off principal will always lower interest charges, but the gains are multiplied over the life of the debt.

Obviously, things are going to be a lot more fun at the end of the loan than at the beginning, but paying a few extra dollars into your note early-on will reap impressive benefits later.

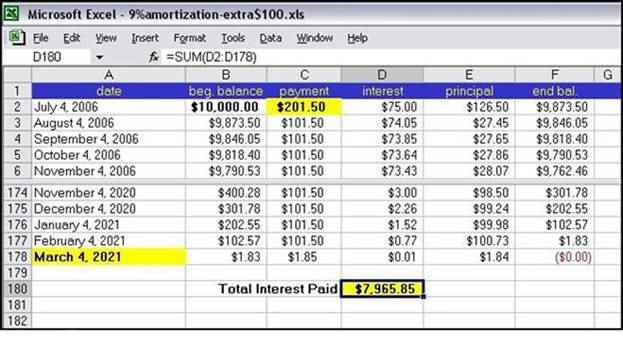

Just to demonstrate exactly how impressive, let’s start out by making an extra $100 payment at the very beginning of the loan. That is, when you make out the check for your first payment, in this case instead of making the regular payment $101.50, you pay $201.50.

Here’s what the amortization schedule looks like:

Now let’s see how much good that extra $100 did for us. Plenty. Fifteen years later, at the end of the loan you’ve saved $280.95 in interest paid, and you’ve retired your debt three months early! All this for a hundred bucks.

So you can see that, if you can pay a bit more than the program calls for, you can save yourself a nice bit of change.

Now that you’ve got the hang of how it works, let’s investigate the three strategies to save on interest.

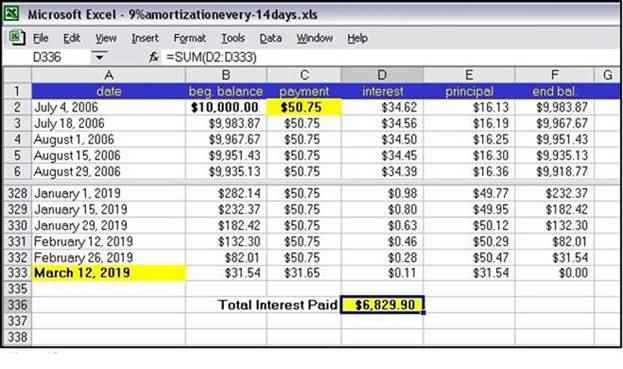

#1 Switch to Bi-weekly Payments Saves 815 days and $1,412

How it’s done: Instead of making the regular monthly payments according to the amortization schedule, you make half a payment every two weeks.

What it costs: Making half a payment twice per month doesn’t in itself cost anything and will save you $188 or so over the fifteen-year term. What we’re doing, however is paying every 14 days so that, because there are enough weeks in the year to make up thirteen months, you actually pay one extra month’s payment per year more than you’re scheduled to.

The Results: Paying every fourteen days, you pay your loan off 2¼ years early and you save $1,412.35 in interest fees.

Hint: You might also want to consider that you’ll be making 180 more payments which might incur other costs, like postage or credit card fees. These days, many lenders offer on-line payment options.

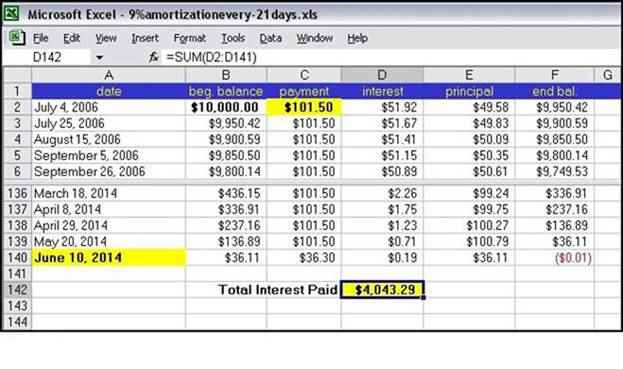

#2 Make a Payment Every Three Weeks. Saves 2,551 days and $4,199

How it’s done: Instead of making the regular monthly payments according to the amortization schedule, you pay the monthly amount every 21 days. It feels like a monthly payment, but you’re speeding your payback considerably.

What it costs: You make 5-1/3 more payments ($541) in a year’s time than you would paying the regular monthly amortization.

The Results: Paying every three weeks, you pay your loan off seven years early, and you save $4,198.96.

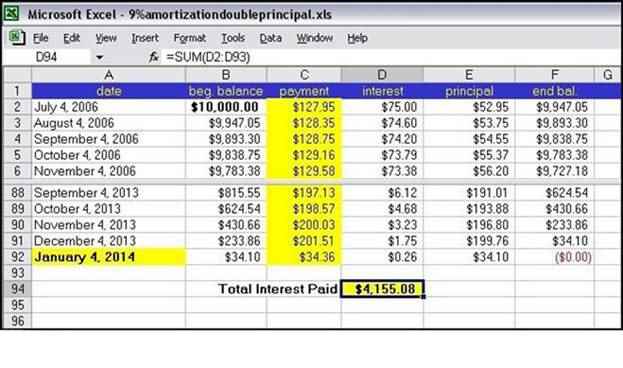

#3 Double Up on Your Principal Payments Saves 2,709 days and $4,087

How it’s done: Print out an amortization schedule for your loan. Each time you make a payment for the current month, include next month’s principal amount in the check as well. Then cross both months off the list. Each time you do this, you save yourself a month over the amortization schedule.

What it costs: At first, your payments are only a bit higher than the regular amortization, in the case given, the first month’s payment goes from $101.50 to $127.95 whereas your last few payments before your early pay-off are nearly twice what the original monthly payment was.

The Results: Paying double principal payments, you pay your loan in half the time (7½ years) and you save $4,087.17.

It’s important to remember when making advance payments, that even if you’re paid a year ahead, you’re still obligated to make the monthly payments unless you’ve made other arrangements with your lender.

~~~~~~~~~~

Read more from Neil:

Throwing in the Towel: How to Move to the Country Fast and Cheap

There is Only One Way, DAMMIT, to Pronounce “Missouri”!

How to Sell Your Land Yourself and Move on with Your Life

Mortgage Free! Radical Strategies for Home Ownership By Rob Roy